Deploying Institutional Liquidity on Bitcoin

This report shares the latest information regarding UTXO Management activities, a brief overview of the Bitcoin ecosystem landscape over the quarter, and updated data about our investments. Each edition is accompanied by commentary from UTXO employees sharing exclusive insights based on their role within the fund.

This edition features Henry Elder, who provides readers with an overview of how UTXO is pioneering on-chain capital deployment as an investment fund and describes how to evaluate yield-generating strategies within the Bitcoin L2 space.

The information contained herein has been provided to you by UTXO Management, LLC and its affiliates (“UTXO Management”) solely for informational purposes. Neither the information, nor any opinion contained herein, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options, coins or other financial instruments. Nothing contained herein constitutes investment, legal or tax advice or is an endorsement of any of the companies, digital currencies, or coins mentioned herein. You should make your own investigations and evaluations of the information herein, as it may not be independently verified by UTXO Management. UTXO Management, its affiliates, funds and principals may have financial exposure to the companies, digital currencies and investment themes mentioned.

Quarterly Macro State of Bitcoin Investing

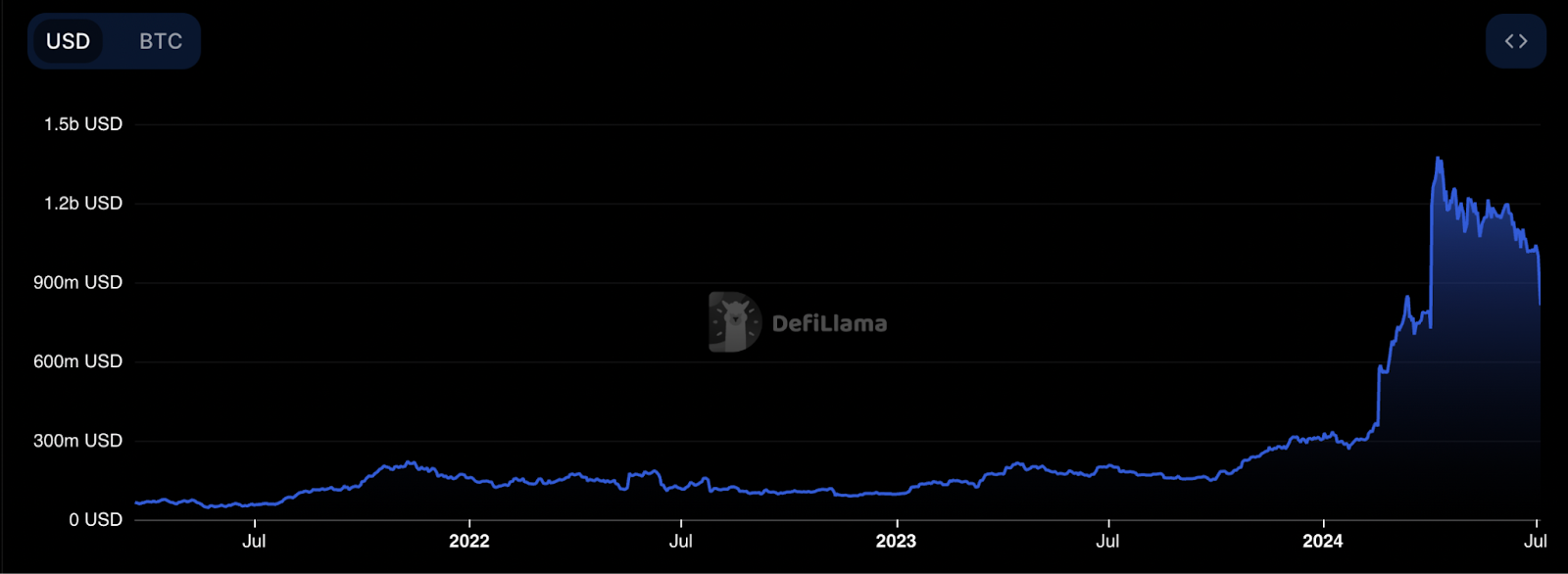

Frontrunning the Future: Bitcoin L2s and the Stickiness of TVL

While Q4 2023 and Q1 2024 were marked by a surge in interest for BitVM and the new possibilities it can enable, Q2 2024 has been a sobering quarter for most market participants. Valuations have cooled down and new research initiatives have helped make sense of what is happening on Bitcoin. We are on the verge of a possible new bull market for Bitcoin coupled with a reinvigorated sense of purpose among developers looking to build new, exciting applications on top of Bitcoin. Within the next 18 months, Bitcoin is going to become a competitor to ETH and Solana both in terms of programmability and ease of use.

Despite being an incomplete and often misleading metric, Total Value Locked (TVL) can sometimes provide insight into the market’s appetite to put digital assets to use. While TVL across Bitcoin L2s skyrocketed in Q1 and the first few weeks of Q2, Q2 marked a dramatic downturn in the trend. TVL across major Bitcoin L2s decreased from $1.32B on April 9th to $800M at the time of writing. So what went wrong?

Stickiness — or rather the lack thereof. Most projects have chosen to adopt incentive structures and go-to-market strategies common in other ecosystems, forgetting that building on Bitcoin is different. Most of the capital in crypto is mercenary capital, meaning it will readily be transferred from one protocol to the next with one goal: maximize returns.

Does that mean that Bitcoin sidechains are doomed to fail? On the contrary — early Bitcoin sidechains that have a first-mover advantage and can attract more meaningful TVL because of their capacity to render BTC useful won’t have to rely as much on incentives, and will be able to organically grow their userbase. We expect this differentiation to happen between Q3 and Q4 2024.

A Post-Mortem on Runes and the Ordinals Ecosystem

Coming off all-time highs for Bitcoin and entering the Halving month, the entire ecosystem was fertile ground for euphoria and big expectations. Blue-chip Ordinal collections like Pups and NodeMonkes outperformed everything. Before the halving, the pre-Runes narrative allowed traders to express a view on the potential of Runes, resulting in many tokens skyrocketing in value. However, the initial response to Runes didn’t match pre-launch expectations. The community realized that Runes was, at best, a marginal improvement upon the BRC-20 standard instead of the promised paradigm change.

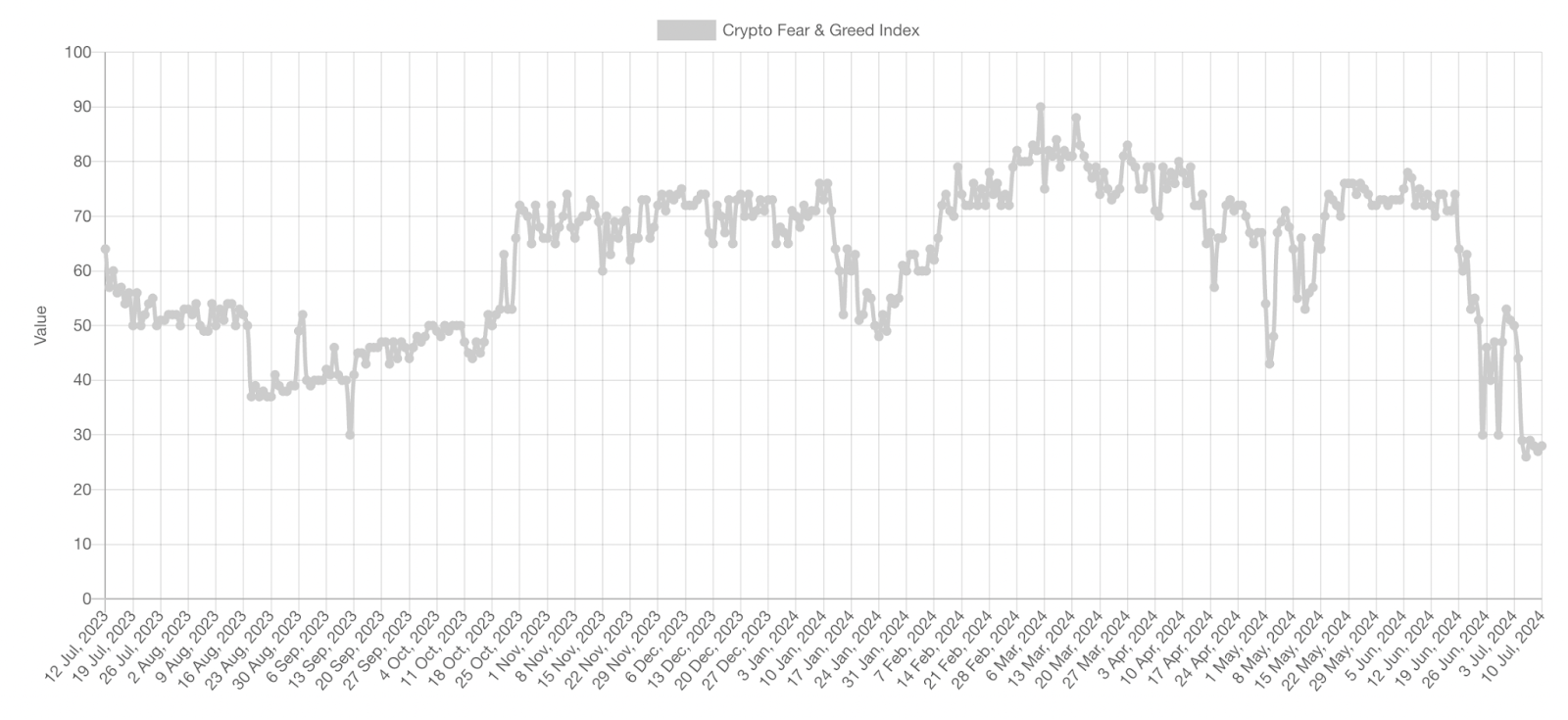

We started the quarter with Greed, and we’re ending with Fear. The Crypto Fear and Greed Index, typically used to gauge investor sentiment, started around 80 at the beginning of Q2 2024 and ended around 30 — a level not seen since September 2023.

While the summer is typically a period of sideways price action for Bitcoin and equities, the asymmetry of the Runes bet remains hard to ignore. The total market cap of Runes remains under $2B (with around 50% being DOG), with no Runes listed on major exchanges. For reference, the marketcap of all meme tokens on Solana is around $6.2B, while the marketcap of frog-themed tokens is around $5.2B. If history repeats itself, a wave of listings could spark a new bull run for the ecosystem, similar to what happened in 2023 with BRC-20s and ORDI on Binance.

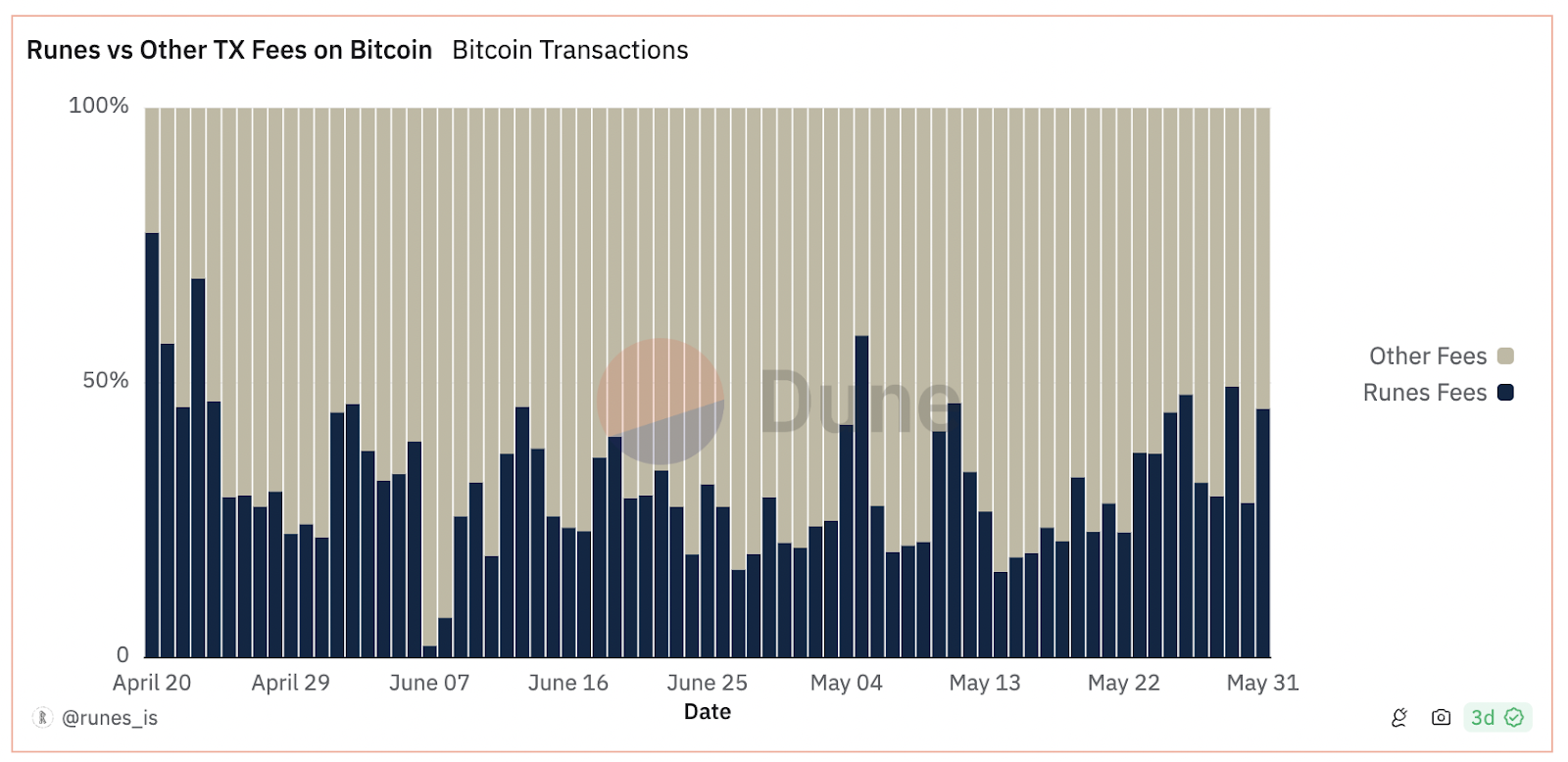

On-chain data is also here to support this thesis. Even as the price of most Runes has declined, they continue to represent close to 50% of all on-chain activity on Bitcoin in terms of transaction fees. UTXO will continue to make investments both into Runes and Runes infrastructure — we believe that tokens on Bitcoin are here to stay.

Furthermore, data from GeniiData about Liquidium showcases that Runes are slowly outpacing the number of Ordinals being used as collateral on the Bitcoin-native lending protocol. The backbone of the ecosystem is slowly moving to become one of the Runes standard.

The Success of Metaplanet — Running the MicroStrategy Playbook

Early in the quarter, UTXO made an investment into Metaplanet. The success was immediate, with the stock price opening Q2 at 20 JPY and closing at 100 JPY by the end of the quarter. UTXO is proud to support a renewed interest in Bitcoin as the ultimate treasury asset among public companies.

As of July 8, Metaplanet holds ~203.73 bitcoin acquired for ¥2.05 billion at an average price of ¥10,062,517 per BTC. As Metaplanet adopts its Bitcoin strategy, the goal is to enhance shareholder value through strategic, perpetual Bitcoin accumulation. The strategic roadmap encompasses various financial tactics, including equity financing considerations and long-dated fiat currency market arbitrage, all executed within a Bitcoin-centric framework.

Since then, UTXO has been approached by dozens of companies looking to replicate Metaplanet’s strategy and adopt Bitcoin as a treasury asset. We’ll continue to monitor attractive opportunities with the goal of getting every company “off-zero” with their Bitcoin treasuries.

*Tyler Evans has been appointed to the Board of Directors of Metaplanet as an Independent Director.

Publicly Disclosed Investments in Q2 2024

- BitLayer

- Metaplanet

- Arch Network

- Ord.io

- SatScreener

- SatRepublic

- Botanix Labs

- UXUY

- Bitcoin Layers

- BAMK.fi

- Lava

- Ordinox

- Rebar Labs

- QED Protocol

During the quarter, we also published our investment thesis describing Bitcoin as the Settlement Chain for all economic activity.

On-Chain Capital Deployment

Henry Elder is a Principal at UTXO Management, managing the Bitcoin Decentralized Finance (DeFi/BTCfi) portfolio. He has been investing in Bitcoin since 2016 and was previously Head of DeFi at Wave Digital Assets, leading separate DeFi ecosystem funds for Polygon, Cardano, Horizen, and Hedera.

How We’re Pioneering On-Chain Capital Deployment

Throughout the entire history of digital assets, Bitcoin has held the distinction of being the most desirable of the asset class. Yet Bitcoin holders wishing to generate yield were typically required to pursue one of two custodial (trusted) options:

- Lend BTC to counterparties via centralized entities such as Genesis or Galaxy.

- Wrap BTC into an ERC-20 token via depositing the BTC at BitGo.

During this time, Ethereum developed a sprawling decentralized finance ecosystem that enabled the creation of sophisticated financial products that minimized counterparty risk. Wrapped BTC was adopted early in this ecosystem, but it did not find significant product market fit with Bitcoin holders — leading to less than 0.01% of all bitcoin being wrapped. This period coincided with an entrenched conservative mindset within the bitcoin ecosystem that eschewed innovation or cooperation with other chains.

Bitcoin began to emerge from this innovation “Dark Age” in mid-2023, and by 2024 had a nascent but flourishing ecosystem of decentralized finance (“BTCfi”) and Layer-2 blockchains anchored in the Bitcoin ethos. This new BTCfi ecosystem ports over many of the trustless models for financial products developed on Ethereum, giving Bitcoiners access to native yield opportunities for the first time.

Dominating the Leaderboards

UTXO has been at the forefront of this BTCfi Renaissance, testing blockchains, applications, and strategies. The fund has become the most recognizable institution in BTCfi, drawing deal flow and new opportunities. We are operating a validator for Core Chain, and supplying liquidity to Core, BoB, and Mezo.

Understanding Yield-Generating Strategies in the Bitcoin L2 Space

Investing in DeFi is a unique process that requires new tools and heuristics to analyze value, execute trades, manage positions, and evaluate risks. The culture of the chain can have a significant impact on the long-term viability and corresponding value of its DeFi ecosystem. Bitcoin has an inherent benefit in this regard as a chain with a long-established cultural preference for security and careful evaluation of technology. UTXO is committed to furthering those values in recognition of the competitive edge they will provide BTCfi.

BTCfi is in its infancy and can be broadly organized into three categories:

Sidechains

Sidechains were built on top of or alongside Bitcoin with a focus on cultural commitment to Bitcoin but not a strong technological or security link. The Bitcoin sidechains that exist today mostly draw inspiration from existing Ethereum L2 DeFi ecosystems such as Blast or Polygon. Rootstock, Core, BoB, BSquared, and Merlin fall into this camp, each having tenuous technological and security links to Bitcoin and instead opting for an EVM approach, integrating Ethereum assets and tools such as Metamask. Stacks is a notable exception, using a Proof-of-Stake model with its native STX token and the Clarity VM.

Layer-2 Chains

Layer-2 chains attempt to directly benefit from Bitcoin protocol security using various technologies such as ZK rollups. They may use Bitcoin-native assets, Ethereum-native assets, or a mix. Lightning Network, Botanix, Citrea, and Alpen are examples. Other than Lightning, these products are largely still in the development stage.

Bitcoin Metaprotocols

Metaprotocols use the Bitcoin chain directly and are the most Bitcoin-native classification. They use Bitcoin-native assets and operations are encoded directly into Bitcoin blocks (decoded via custom indexers). Arch Network is an example supporting BTCfi applications; Ordinals, BRC-20s, and Runes are also metaprotocols — they simply support BTCfi assets.

Quantifying the Opportunity for True Native Bitcoin Yield

Bitcoin is the only crypto asset with universal appeal. It is now recognized, understood, and trusted throughout the crypto world, retail tradfi world, and institutional tradfi world. This drives great demand for usage as a collateral asset, trade settlement asset, and money. However, the lack of programmability and lack of a native financial ecosystem has relegated Bitcoin to primarily meeting that demand through centralized entities.

ETH has historically dominated demand for on-chain crypto asset financialization, with $115B worth of ETH staked to secure the Ethereum network and $35B further restaked to secure other networks. ETH is also the most widely-used collateral asset on-chain. ETH staking and restaking provide the equivalent “risk-free rate” for crypto. This entire use case will likely be subsumed by Bitcoin, which is a superior collateral asset and is rapidly catching up on relevant technological metrics.

Bitcoin also has a superior cultural component: it hasn’t historically been viewed as a competitor to most smart-contracting blockchains. The deeply partisan relationships between Ethereum, Solana, Cardano, Tron, and others do not exist to the same degree with Bitcoin. Each of those chains uses its own base asset to bootstrap security and continually dilutes holders through high inflation — a massive cost that means most blockchains are unprofitable the majority of the time. Layer 2 technologies demonstrate that a chain with a unique asset can exist on top of a far more secure Layer 1 and reduce security costs by 10–100x.

The only real Layer 1 option to build on has been Ethereum, which is culturally impossible for legacy competitors like Cardano, Polkadot, Cosmos, Avalanche, Tron, BNB, and Solana. Bitcoin now offers an alternative that is economically more secure, credibly neutral, and potentially offers superior technological security by dint of a lower attack surface. Legacy projects can remove billions of dollars of annual expenses and inflation by moving to a proof-of-stake model using BTC or an L2 directly on top of Bitcoin.

Managing Risk When You’re Early

DeFi is similar to traditional lending in that the biggest single risk is usually your counterparty — in this case, the decentralized application itself. History shows that a hack of the application often results in the total loss of principal. Diversification can be a useful tool to counter this risk, but DeFi requires other, new frameworks to evaluate risks as well. The underlying technology is usually more relevant than the balance sheet. Your returns can be denominated in a range of cryptocurrencies that each come with unique risks — tokenomics, tech risks, and founder/product quality.

Custody solutions are highly fragmented, with best practices defined by the capability and product availability on each blockchain. Crisis situations can happen in a literal instant, forcing asset managers to react instinctively. The risk/reward for vanilla liquidity provisioning is often unattractive compared to the additional incentives that a large LP can extract. Together, these factors have led to a decline in retail LP as efficiencies in risk management and incentive extraction accrue to institutional investors.